WEEKLY RINGGIT BOND MARKET SNAPSHOT between 27/07/2026 to 31/07/2026

FTSE BPAM Bond Index Series

|

|

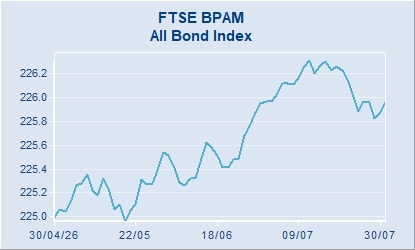

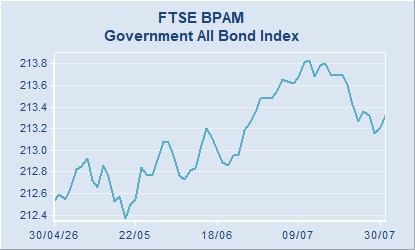

| Index Value (This Week Close): | 225.955 | Index Value (This Week Close): | 213.320 |

| Index Value (Last Week Close): | 225.884 | Index Value (Last Week Close): | 213.271 |

| Week On Week Change: | 0.071  | Week On Week Change: | 0.049 |

| % Change: | 0.031 % | % Change: | 0.023 % |

| |

|

|

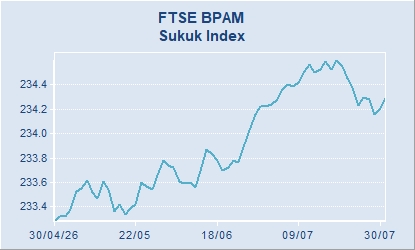

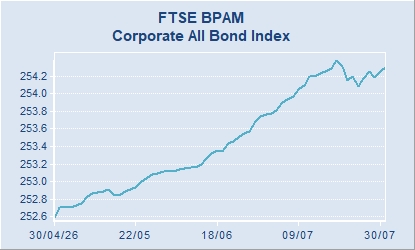

| Index Value (This Week Close): | 234.289 | Index Value (This Week Close): | 254.299 |

| Index Value (Last Week Close): | 234.232 | Index Value (Last Week Close): | 254.078 |

| Week On Week Change: | 0.057 | Week On Week Change: | 0.221 |

| % Change: | 0.024 % | % Change: | 0.087 % |

| |

|

Constant Maturity YTM Curve

|

Constant Maturity Conventional Yield-To-Maturity

| 3.103 |

3.239 |

3.354 |

3.509 |

3.660 |

3.752 |

3.954 |

3.992 |

4.058 |

4.127 |

| 3.300 |

3.417 |

3.523 |

3.670 |

3.807 |

3.910 |

4.073 |

4.173 |

4.223 |

4.267 |

| 3.500 |

3.610 |

3.680 |

3.770 |

3.870 |

3.990 |

4.140 |

4.240 |

4.300 |

4.360 |

| 3.620 |

3.740 |

3.800 |

3.890 |

3.980 |

4.110 |

4.320 |

4.540 |

4.710 |

4.830 |

| 4.600 |

4.920 |

5.200 |

5.610 |

5.920 |

6.340 |

6.930 |

7.420 |

7.790 |

8.110 |

| 6.090 |

6.660 |

7.120 |

7.800 |

8.350 |

9.030 |

9.850 |

10.590 |

11.280 |

11.920 |

|

Constant Maturity Islamic Yield-To-Maturity

| 3.120 |

3.225 |

3.325 |

3.532 |

3.651 |

3.762 |

3.969 |

3.995 |

4.061 |

4.127 |

| 3.300 |

3.417 |

3.523 |

3.670 |

3.807 |

3.910 |

4.073 |

4.173 |

4.223 |

4.267 |

| 3.500 |

3.610 |

3.680 |

3.770 |

3.870 |

3.990 |

4.140 |

4.240 |

4.300 |

4.360 |

| 3.620 |

3.740 |

3.800 |

3.890 |

3.980 |

4.110 |

4.320 |

4.540 |

4.710 |

4.830 |

| 4.600 |

4.920 |

5.200 |

5.610 |

5.920 |

6.340 |

6.930 |

7.420 |

7.790 |

8.110 |

| 6.090 |

6.660 |

7.120 |

7.800 |

8.350 |

9.030 |

9.850 |

10.590 |

11.280 |

11.920 |

|

| Back to Top |

YTM Spread (This week - last week's closing)

|

| Back to Top |

This Week Most Active Bonds

| GII MURABAHAH 3/2016 4.070% 30.09.2026 |

NR(LT) |

4,706 |

2.971 |

3.030 |

2.978 |

| MGS 3/2016 3.900% 30.11.2026 |

NR(LT) |

2,267 |

2.978 |

2.994 |

2.946 |

| GII MURABAHAH 3/2026 3.227% 15.10.2029 |

NR(LT) |

2,120 |

3.349 |

3.328 |

3.242 |

| MGS 2/2025 3.476% 02.07.2035 |

NR(LT) |

1,407 |

3.701 |

3.697 |

3.600 |

| MGS 2/2019 3.885% 15.08.2029 |

NR(LT) |

1,097 |

3.350 |

3.323 |

3.273 |

| MGS 4/2013 3.844% 15.04.2033 |

NR(LT) |

1,002 |

3.648 |

3.632 |

3.533 |

| GII MURABAHAH 1/2023 3.599% 31.07.2028 |

NR(LT) |

945 |

3.280 |

3.257 |

3.220 |

| MGS 2/2023 3.519% 20.04.2028 |

NR(LT) |

735 |

3.235 |

3.238 |

3.173 |

| GII MURABAHAH 1/2022 4.193% 07.10.2032 |

NR(LT) |

647 |

3.636 |

3.576 |

3.521 |

| MGS 3/2007 3.502% 31.05.2027 |

NR(LT) |

641 |

3.101 |

3.121 |

3.093 |

| PRASARANA IMTN 3.620% 31.07.2031 (SERIES 30) |

NR(LT) |

600 |

3.620 |

- |

- |

| PRASARANA IMTN 4.050% 11.10.2033 - Series 1 |

NR(LT) |

70 |

3.809 |

3.792 |

3.756 |

| PRASARANA IMTN 4.110% 27.08.2036 (Series 3) |

NR(LT) |

70 |

3.874 |

3.846 |

3.810 |

| CAGAMAS IMTN 4.120% 05.10.2028 |

AAA |

40 |

3.495 |

3.506 |

3.476 |

| BPMB GG IMTN 4.75% 12.09.2029 - ISSUE NO 5 |

NR(LT) |

15 |

3.516 |

3.503 |

3.448 |

| CAGAMAS MTN 3.800% 06.12.2027 |

AAA |

15 |

3.349 |

3.329 |

3.335 |

| PTPTN IMTN 3.630% 10.09.2038 (Series 2) |

NR(LT) |

15 |

3.959 |

3.908 |

3.883 |

| CAGAMAS IMTN 3.730% 06.05.2033 |

AAA |

10 |

3.836 |

3.809 |

3.787 |

| PASB IMTN 3.700% 06.06.2028 - Issue No. 38 |

NR(LT) |

1 |

3.362 |

3.356 |

3.325 |

| MAYBANK IMTN 3.100% 08.10.2032 |

AA1 |

200 |

3.651 |

3.632 |

3.614 |

| PSEP IMTN 3.700% 07.08.2035 (Tr5 Sr3) |

AAA |

200 |

3.932 |

3.909 |

3.898 |

| PSEP IMTN 3.900% 24.05.2027 (Tr4 Sr1) |

AAA |

180 |

3.463 |

3.468 |

3.449 |

| TENAGA IMTN 3.810% 27.05.2033 |

AAA |

140 |

3.799 |

3.781 |

3.771 |

| MRCB20PERP IMTN Issue 9-S2 4.350% 08.07.2033 |

AA- IS |

120 |

3.984 |

4.018 |

- |

| OSK RATED IMTN 4.120% 02.03.2035 (Series 007) |

AA IS |

120 |

4.006 |

4.019 |

3.993 |

| MRCB20PERP IMTN Issue 8-19 4.390% 10.04.2034 |

AA- IS |

110 |

3.965 |

4.037 |

4.091 |

| MRCB20PERP IMTN Issue 9-S3 4.390% 10.07.2034 |

AA- IS |

91 |

3.986 |

4.056 |

- |

| MRCB20PERP IMTN Issue 8-20 4.410% 10.04.2035 |

AA- IS |

90 |

4.015 |

4.081 |

4.117 |

| CIMB 4.000% 12.08.2038-T2 Sukuk Wakalah S8 T2 |

AA2 |

85 |

4.092 |

4.043 |

4.025 |

| CIMBI IMTN 4.070% 30.07.2035 - Series 4 Tranche 3 |

AAA IS |

80 |

3.919 |

3.907 |

3.865 |

| MRCB20PERP IMTN Issue 7-15 4.250% 30.01.2036 |

AA- IS |

80 |

4.059 |

4.102 |

4.149 |

| TENAGA IMTN 27.08.2038 |

AAA |

80 |

3.989 |

3.989 |

3.987 |

| PBAPP IMTN 3.570% 3652D 04.09.2035 |

AAA |

75 |

3.931 |

3.916 |

3.887 |

| CIMBI IMTN 4.130% 27.03.2034 - Series 3 Tranche 4 |

AAA IS |

70 |

3.858 |

3.857 |

3.826 |

| MUAMALAT TIER 2 SUKUK WAKALAH 4.150% 26.05.2036 |

A IS |

70 |

4.077 |

4.099 |

4.095 |

| MRCB20PERP IMTN Issue 8-18 4.350% 08.04.2033 |

AA- IS |

60 |

3.968 |

4.016 |

4.068 |

| YTL POWER IMTN 4.620% 24.08.2035 |

AAA |

60 |

4.017 |

4.121 |

3.914 |

| MEX I IMTN TRANCHE 14 21.01.2038 |

AA2 |

52 |

4.118 |

4.129 |

4.112 |

| MRCB20PERP IMTN Issue 6-12 4.020% 28.11.2030 |

AA- IS |

50 |

3.927 |

3.963 |

3.959 |

|

| Back to Top |

Upcoming New Issues

| PLB MTN 1283D 07.2.2030 |

04/08/2026 |

5Y |

70 |

AA |

MTN |

| SFSB IMTN 01.04.2030 Tranche 7C-3 |

03/08/2026 |

5Y |

4 |

NR(LT) |

MTN |

| SFSB IMTN 01.04.2030 Tranche 7B-3 |

03/08/2026 |

5Y |

2 |

NR(LT) |

MTN |

| SETIAALAMSA IMTN FLOATING RATE 28.01.2030 |

03/08/2026 |

5Y |

14 |

NR(LT) |

MTN |

| SFSB IMTN 01.04.2030 Tranche 7A-3 |

03/08/2026 |

5Y |

2 |

NR(LT) |

MTN |

| AIR SELANGOR IMTN T9 SRI (BLUE) 4.33% 02.08.2041 |

03/08/2026 |

15Y |

200 |

AAA |

MTN |

| CAGAMAS CP-CPN 3.500% 364D 05.08.2027 |

06/08/2026 |

1Y |

300 |

P1 |

CP |

| CAGAMAS ICP-CPN 3.43% 92D 05.11.2026 |

05/08/2026 |

3M |

200 |

P1 |

CP |

| F&NCAP ICP 57D 29.09.2026 |

03/08/2026 |

3M |

90 |

MARC-1 IS (CG) |

CP |

| PASB ICP 184D 03.02.2027 - Tranche 5 |

03/08/2026 |

6M |

720 |

P1 |

CP |

|

| Back to Top |

Upcoming Maturing Issues

| SABAHDEV MTN 1096D 03.8.2026 - Issue No. 213 |

03/08/2026 |

3Y |

84 |

AA1 |

MTN |

| PLB MTN 1098D 04.8.2026 |

04/08/2026 |

3Y |

50 |

AA |

MTN |

| JELAS PURI MTN 365D 05.8.2026 (SERIES 1) |

05/08/2026 |

1Y |

3 |

NR(LT) |

MTN |

| PAB ABSMTN CLASS B JUNIOR MTN T1 1096D 03.8.2026 |

03/08/2026 |

3Y |

171 |

NR(LT) |

ABS(MTN) |

| CAGAMAS ASEAN SOCIAL SRI 3M KLIBOR+0.02% 05.08.26 |

05/08/2026 |

1Y |

200 |

AAA |

MTN |

| PRASARANA IMTN 0% 04.08.2026 - MTN 4 |

04/08/2026 |

15Y |

1,200 |

NR(LT) |

MTN |

| QSR STORES IMTN 03.08.2026 - Tranche 2 |

03/08/2026 |

2Y |

0 |

NR(LT) |

MTN |

| TGJH IMTN 07.08.2026 (Tranche 1 Series 3) |

07/08/2026 |

5Y |

6 |

NR(LT) |

MTN |

| TH1 IMTN 4.950% 06.08.2026 (Series 4) |

06/08/2026 |

7Y |

20 |

A1 |

MTN |

| MRL ICP 181D 06.08.2026 |

06/08/2026 |

6M |

1,050 |

NR(ST) |

CP |

| F&NCAP ICP 181D 04.08.2026 |

04/08/2026 |

6M |

90 |

MARC-1 IS (CG) |

CP |

| EXSIM ICP 181D 06.08.2026 (ICP4 T7 IMTN) |

06/08/2026 |

6M |

8 |

NR(ST) |

CP |

|

| Back to Top |

Tender Results

| MGS 1/2026 3.766% 15.01.2041 |

21/07/2026 |

22/07/2026 |

3,500 |

98.492 |

3.903 |

MGS |

| MTB 6/2026 183D 15.01.2027 |

15/07/2026 |

16/07/2026 |

1,500 |

98.481 |

3.080 |

MTB |

| GII MURABAHAH 3/2026 3.227% 15.10.2029 |

14/07/2026 |

15/07/2026 |

5,000 |

99.814 |

3.287 |

GII |

| MTB 5/2026 183D 08.01.2027 |

08/07/2026 |

09/07/2026 |

1,500 |

98.489 |

3.060 |

MTB |

| MGS 2/2025 3.476% 02.07.2035 |

02/07/2026 |

03/07/2026 |

5,000 |

98.830 |

3.630 |

MGS |

| GII MURABAHAH 4/2025 3.775% 31.05.2045 |

25/06/2026 |

26/06/2026 |

3,000 |

97.094 |

3.995 |

GII |

| MGS 4/2011 4.232% 30.06.2031 |

19/06/2026 |

22/06/2026 |

5,000 |

103.628 |

3.439 |

MGS |

| GII MURABAHAH 1/2025 3.974% 16.07.2040 |

12/06/2026 |

15/06/2026 |

3,500 |

100.816 |

3.898 |

GII |

| MTB 4/2026 365D 11.06.2027 |

10/06/2026 |

11/06/2026 |

500 |

100.000 |

3.130 |

MTB |

| MGS 2/2026 3.237% 15.03.2029 |

04/06/2026 |

05/06/2026 |

5,000 |

99.981 |

3.243 |

MGS |

| GII MURABAHAH 1/2026 4.044% 31.01.2056 |

28/05/2026 |

29/05/2026 |

3,000 |

98.993 |

4.103 |

GII |

| MGS 4/2013 3.844% 15.04.2033 |

21/05/2026 |

22/05/2026 |

5,000 |

101.600 |

3.580 |

MGS |

| GII MURABAHAH 3/2025 3.612% 30.04.2035 |

14/05/2026 |

15/05/2026 |

5,000 |

100.089 |

3.600 |

GII |

| MGS 3/2026 3.987% 23.04.2046 |

22/04/2026 |

23/04/2026 |

3,500 |

100.000 |

3.987 |

MGS |

| GII MURABAHAH 3/2026 3.227% 15.10.2029 |

14/04/2026 |

15/04/2026 |

5,000 |

100.001 |

3.227 |

GII |

| MITB 4/2026 365D 13.04.2027 |

10/04/2026 |

13/04/2026 |

1,500 |

100.000 |

3.120 |

MTB |

| MGS 3/2025 3.917% 15.07.2055 |

07/04/2026 |

08/04/2026 |

3,000 |

95.299 |

4.197 |

MGS |

| MTB 3/2026 365D 06.04.2027 |

03/04/2026 |

06/04/2026 |

2,000 |

100.000 |

3.140 |

MTB |

| MITB 3/2026 91D 02.07.2026 |

01/04/2026 |

02/04/2026 |

2,500 |

99.267 |

2.960 |

MTB |

| GII MURABAHAH 2/2026 3.624% 31.03.2033 |

30/03/2026 |

31/03/2026 |

5,000 |

100.000 |

3.624 |

GII |

|

| Conv |

Conventional principle |

| Islm |

Islamic principle |

| MGS |

Malaysian Government Securities. Conventional bonds issued by the Government of Malaysia |

| GII |

Government Investment Issue. A sukuk issued by the Government of Malaysia |

| Yield To Maturity (YTM) |

The expected rate of return of a bond with the assumption it is held until the maturity date |

| Quasi-Govt |

An organisation that has a close affiliation with the government or is set up under a government initiative |

| Fair Val |

Bond Pricing Agency Malaysia Sdn Bhd [200401028895 (667403-U)]'s fair valuation |

| YTM Spread |

Difference between this and previous week's YTM |

| N.A. |

Not Available |

| AAA, AA, A and BBB YTM represent Corporate ratings consolidated from RAM & MARC |

| YTM is calculated in Percentage (%) |

|

| Back to Top |

Disclaimer

Information on this page is intended solely for the purpose of providing general information on the

Ringgit Bond market and is not intended for trading purposes. None of the information constitutes a

solicitation, offer, opinion, or recommendation by Bond Pricing Agency Malaysia Sdn Bhd [200401028895 (667403-U)] to buy or sell any security, or

to provide legal, tax, accounting, or investment advice or services regarding the profitability or

suitability of any security or investment. Investors are advised to consult their professional

investment advisors before making any investment decision. Materials provided on this page are provided

on an "as is" basis, and while care has been taken to ensure the accuracy and reliability of the

information provided in this page, Bond Pricing Agency Malaysia Sdn Bhd [200401028895 (667403-U)] provides no warranties or representations

of any kind, either express or implied, including, but not limited to, warranties of title or implied

warranties of fitness for a particular purpose, accuracy, correctness, non-infringement, timeliness,

completeness, or that the information is always up-to-date.

|

The content of this Web site is not controlled by The Edge Communications Sdn. Bhd.

This link is being offered for your convenience and should not be viewed as an endorsement by The Edge Communications Sdn. Bhd. of the content, products or services offered there.

|

|

|